High mortgage rates are still impacting home sales in 2025

Spring usually brings with it open houses, moving vans and new mortgages. But for many would-be homebuyers, this year’s homebuying season felt more like Groundhog Day.

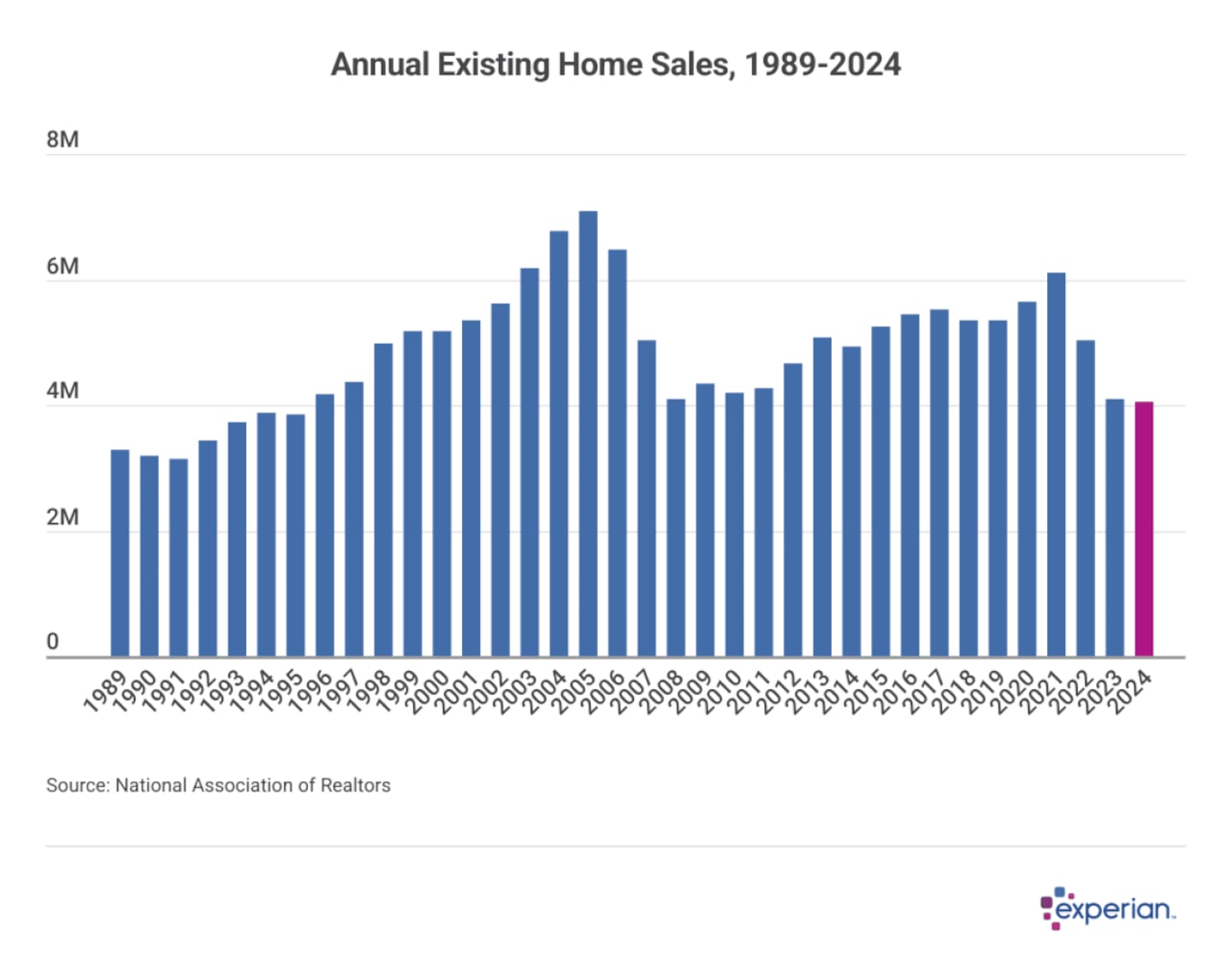

Ever since interest rates for mortgages climbed from 3% following the COVID-19 pandemic to over 6% starting in late 2022, home sales in the U.S. have cooled to a level not seen in decades. Over the past 30 years, it's been typical for more than 5 million homes to change hands annually, according to data from the National Association of Realtors. In 2024, however, barely 4 million homes were bought and sold — the fewest since 1995.

Experian

Not only have “for sale” signs become more rare, but there are now fewer prospective homebuyers checking out properties than in prior years — some perhaps discouraged by the current state of the market. Homes are lingering on the market far longer than they have in recent memory as well. In January, residential real estate company Redfin reported that homes took longer to sell than any time since 2019. Tariff uncertainty will likely extend that timeline even further, at least in the short term.

Although home prices are falling in some markets — particularly in parts of California, Florida and Texas — prices are still climbing in most other residential markets in the U.S.

The reasons for the current home sales slump are multifaceted, but housing supply, insurance, demographics, and macroeconomic conditions all play a role. In this article, Experian focuses on the role mortgage rates have on home sales, as measured by home loan originations.

The Historical Trend: Can Rising Mortgage Rates Explain Home Sale Slumps?

There is a relationship between mortgage financing rates and home prices in the U.S., where most homebuyers finance their purchase with a 30-year fixed-rate mortgage.

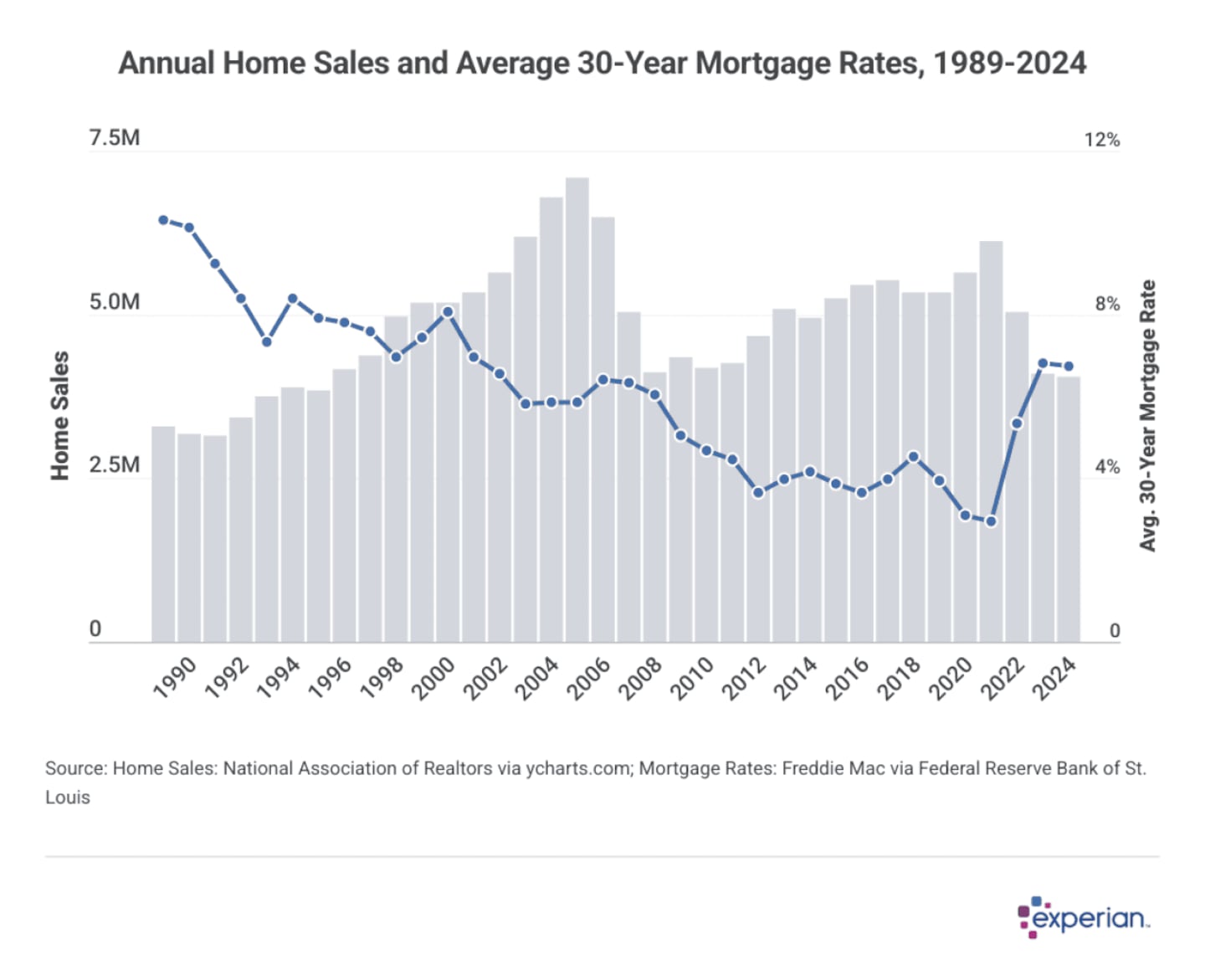

But it may not be the relationship you'd expect. According to a study by the Urban Institute, home price appreciation has historically increased slightly when mortgage rates are higher. This tilt occurs because higher interest rates are typically associated with robust economic growth, and rate cuts are often the result of central banks seeking to stimulate a slowing economy.

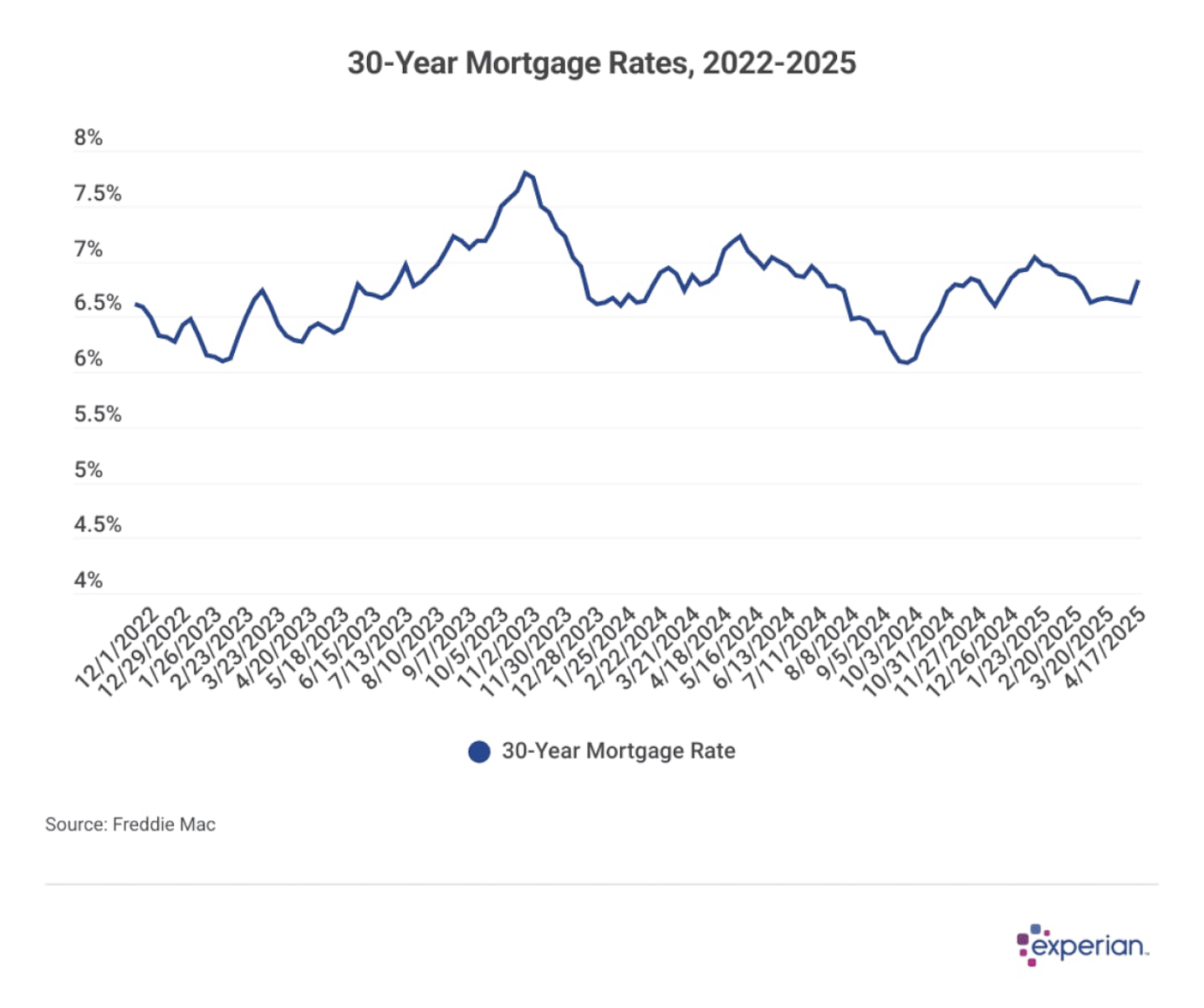

As we were reminded last fall, however, Federal Reserve interest rate cuts don't necessarily lead to lower mortgage rates the same way they would for, say, credit cards. In fact, since the first rate cut in September 2024, mortgage rates have barely budged — if anything, they've trended slightly higher in the months following the cuts.

You can extend the line back even further. Ever since the 10 interest rate hikes executed by the Federal Reserve from 2022 to 2024, mortgage rates have remained stuck in a narrow, elevated range from near 6% at the lowest to almost 8% at the high end.

Experian

Indeed, there are recent instances where declining mortgage rates boosted home sales: It occurred that way for most of the 21st century. As rates declined from 8% in 2000 to below 3% during the height of the pandemic, home sales generally increased. Notably, however, home sales were interrupted for a few years by a little thing known as the Great Recession.

Experian

Challenges Likely to Persist for Homebuyers

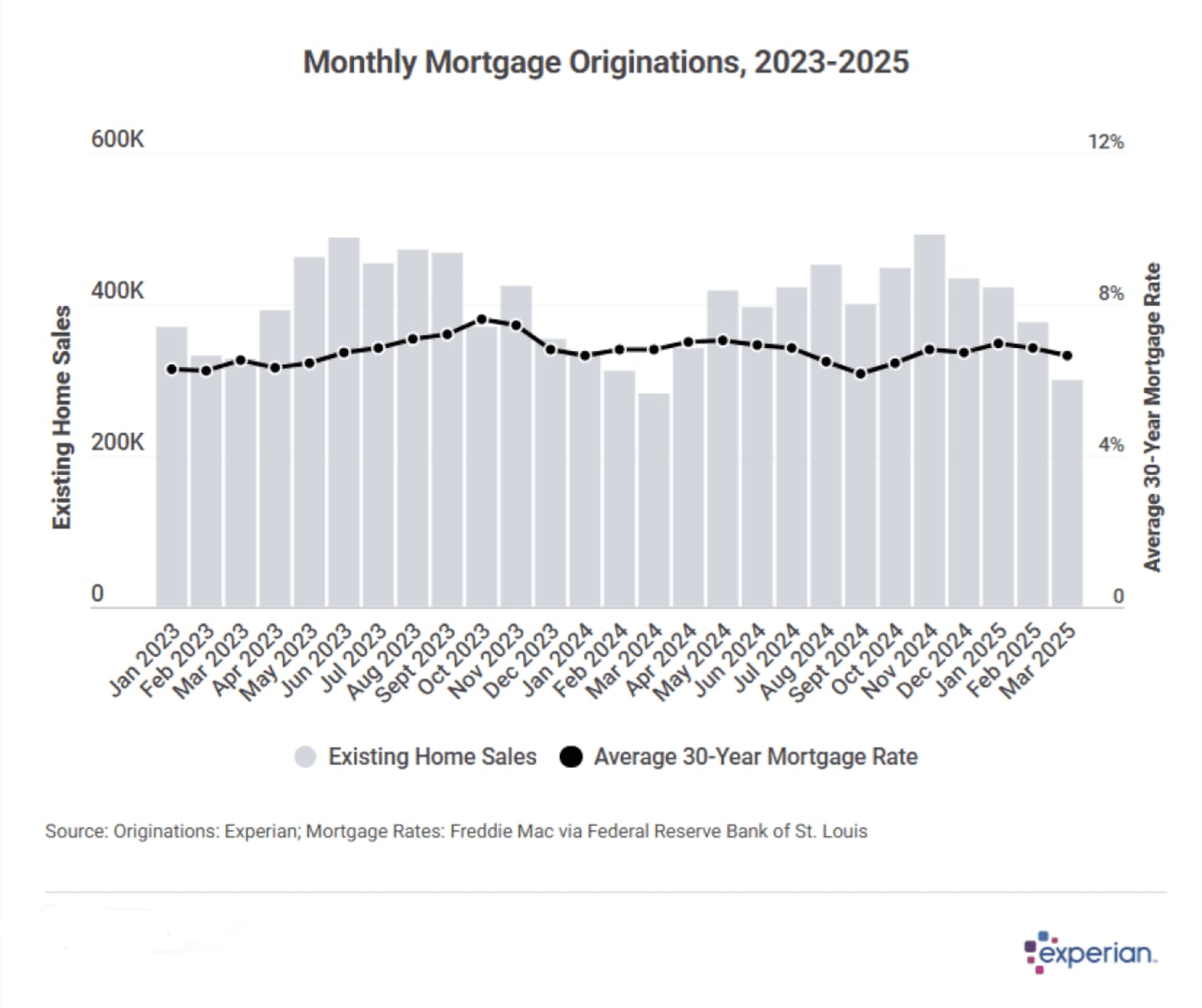

When mortgage rates climbed from those ultra-low mortgage rate levels several years ago, it wasn't surprising to see home sales volume decline. Quick math reveals the increase in mortgage rates from 3% to 6% increases a homebuyer's average monthly mortgage payment by 34%, from $1,657 to $2,227.

Even if buyers were willing to tighten their belts to unhealthy levels in order to make payments, underwriters of mortgages wouldn't be willing to make loans where most of a homeowner's after-tax income services their debt payments.

Experian

Elevated mortgage rates mean persistently higher mortgage costs for prospective homebuyers, some of whom are being priced out of the market entirely under these conditions.

Looking forward to the rest of 2025 and beyond, mortgage rates will likely stay relatively unchanged unless the Federal Reserve gets more aggressive with its rate cuts than the one percentage point already made. With whiffs of inflation still in the air, however, the Fed has signaled that it's unlikely since reducing rates could reignite price hikes. Meanwhile, a recent downgrade of the U.S. Treasury's credit rating by Moody's will mean more near-term upward pressure on mortgage rates, not downward.

On top of everything we've covered here, there are also the secondary factors buffeting the homebuying market, including:

- The cost of rent: Lower rents mean less incentive to move from renting to owning.

- Cash buyers: All-cash buyers tend to outbid those financing, since they'll be assuming no debt; sellers tend to prefer them too.

- Tariff paralysis: No one wants to make a big decision, families and executives alike, amid all the uncertainty.

- Insurance costs: Sharply rising insurance costs are also factors making homebuying less likely than in some markets this summer.

Unless these factors let up, it's unlikely the conditions buyers (and renters) face will change in the near future. However, despite the pessimistic news facing homebuyers broadly, it's important to understand that home prices are driven more by local economic conditions, not national trends. If the local economy is healthy, then it will attract more workers and create a virtuous and stable cycle of economic growth. In the coming months, everyone will see how large the economic “if” is in impacting local mortgage markets.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO® Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

FICO® is a registered trademark of Fair Isaac Corporation in the U.S. and other countries.

This story was produced by Experian and reviewed and distributed by Stacker.

Sign Up

Sign Up